Deciphering Earnings of Big Names

[4.2024] How to Read Microsoft's Earnings: A Key Business to Understand

Since the start of 2024, Microsoft has maintained its growth from the previous year, becoming the second company to reach a $3 trillion market cap after Apple. The market will put Microsoft to the test when it releases its new earnings report after hours on April 25th, which may impact whether its market value remains above the $3 trillion mark.

As we now turn our attention to Microsoft's earnings report, it is important to identify the indicators that could potentially drive its stock price. By looking at the company's growth trajectory, we can pinpoint some key indicators.

There are two main indicators that companies look towards to drive growth: an increase in revenue and higher profit margins. At a glance, it seems Microsoft has been successful in achieving both.

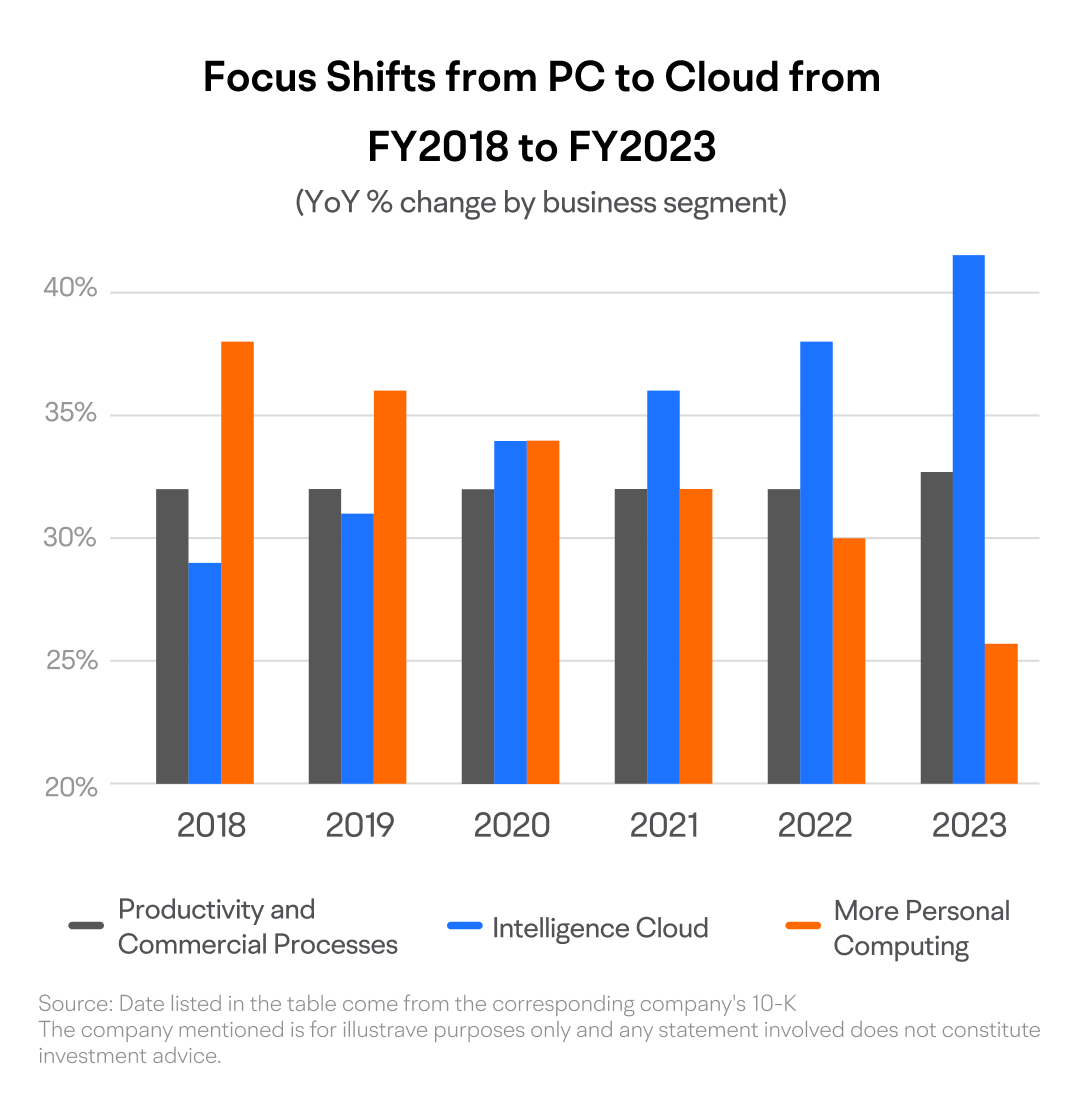

From FY2018 to FY2023, the company has successfully transformed itself from a personal computing manufacturer into a leading cloud computing provider. In its Productivity and Business Processes segment, which includes popular services like Office 365, Microsoft has shifted to a subscription-based model, rather than selling traditional software licenses.

By embracing this new approach, Microsoft has experienced tremendous growth in both revenue and net margin. Between FY2018 and FY2022, its revenue and net margin have almost doubled.

This remarkable performance has translated into a triple net profit, outpacing revenue growth. As a result, Microsoft's stock has risen about 3.3 times since the end of fiscal year 2018.

Microsoft's consistent, steady revenue, and margin growth have played a significant role in its success over the past years. As we analyze the company's quarterly earnings, it is imperative to pay close attention to these key indicators to gain insight into Micorsoft's ongoing performance.

Currently, Microsoft generates its revenue via three major business segments:

While Microsoft's Personal Computing business continues to generate steady revenue, its growth has recently slowed and even turned negative in the past three fiscal quarters. The market does not have high expectations for this segment and therefore the declining revenue growth rate may have less impact on the stock price.

However, Microsoft reported a 2.5% year-over-year growth for this segment in fiscal Q1 2024, which may come as a small surprise. The momentum continued into Q2, with an impressive 18.6% year-over-year increase, indicating a resurgence in PC market demand. In the upcoming financial report, we'll see if the Personal Computing segment can keep up its revenue recovery.

Instead, Intelligent Cloud business has emerged as Microsoft's largest revenue contributor and is now the second-largest cloud provider after Amazon's AWS in terms of market share.

Intelligent Cloud business has maintained an above 20% revenue growth and continued to accelerate this growth between FY2019 and FY2022.

However, Intelligent Cloud's revenue growth dropped quarter over quarter for fiscal 2023, reaching a level of 15%.

A highlight in this area may be Microsoft's advancements in AI are helping to upgrade their cloud business. In the fiscal Q1 2024 earnings report, Microsoft's Intelligent Cloud business showed a rebound in revenue growth with a year-over-year increase of approximately 19%. By Q2 of fiscal year 2024, Intelligent Cloud revenue reached $25.88 billion, marking an approximate 20% year-over-year growth and accelerating the rebound from the previous quarter. In the coming quarters, it remains to be seen whether this trend in revenue growth can be sustained.

The third business segment is productivity and business processes. Subscription revenue from Office 365, Microsoft's leading productivity tool, accounts for most of this segment. Microsoft's office software service underwent a successful transformation about ten years ago, moving from a one-time permanent license sale model to a subscription-based model.

The growth of subscription-based revenue depends on the expansion of the customer base and price increases. Microsoft has historically been reluctant to raise prices, so revenue growth has primarily come from increasing their customer base.

Furthermore, Microsoft's Office suite is characterized by high customer retention and some monopolistic features. The company has high potential to turn its prospective customers into paying clients, while its past customers are inclined to renew their subscriptions.

As a result, growth in this segment has been very stable, moving around 15% for several fiscal years.

However, in the first two quarters leading up to fiscal 2023, revenue from productivity and business processes segment slid to a level of 7%, as businesses sought to lower costs and reduce IT spending. Microsoft later launched Copilot, an AI-powered add-on product to enterprises. According to Microsoft executives on a recent earnings call, as of Q1 fiscal year 2024, over one million paying users have subscribed to the service, with a higher average revenue per user. This has also helped drive growth in revenue of productivity and business processes segment, which reversed in Q3 fiscal year 2023 and continued to rise to a level of 13.2% in Q2 fiscal year 2024.

In upcoming financial seasons, it may be important to monitor the subscription of Copilot and how it contributes to the growth in productivity and business processes segment. This segment may surpass even their Intelligent Cloud business and become the company's biggest highlight, potentially impacting the stock price. As such, it is important to keep a close eye on these developments.

Let's proceed to the second focal point, which is margins. Usually, the net margin serves as the ultimate indicator of profitability. However, it's important to note that in each financial report, Microsoft only discloses the operating profit margins for individual business segments.

From FY2018 to FY2022, Microsoft's data reveals a consistent improvement in operating margins across all business segments.

Among these segments, the Productivity and Business Processes division stands out with the highest margin, and its growth remains stable.

However, the More Personal Computing business experienced a decline since the 2022 fiscal year, which could be attributed to industry cycles and lower market expectations. Its margin improved considerably for fiscal Q1 2024, beating market estimate. Yet, in Q2 of fiscal year 2024, it regressed, possibly defying market expectations.

It's also worth noting that the margin for Microsoft's Intelligent Cloud segment experienced a slight decline in fiscal 2022, and continued to decline in the first three quarters leading up to fiscal 2023.

In Q4 fiscal year 2023, however, Intelligent Cloud's margin rebounded, and it reached historic highs of over 48% for the first two quarters of 2024.

The previous decline may be due to the penetration of the cloud computing industry reaching a certain stage, and intensified competition between companies. Therefore, Microsoft's pricing power may have decreased. The company may have to lower prices or double down on promotional efforts to gain customers.

The substantial rebound in the margin of Intelligent Cloud may be attributed to the improved product competitiveness and bargaining power, thanks to the boost from AI. It remains to be seen whether this high level of profitability can be sustained.

One aspect that deserves close attention is the Copilot add-on, as it has the potential to drive improvements in the average price of Microsoft's Office services. As Copilot's penetration rate increases, Microsoft's productivity and business processes segment, with flagship product Office 365, has seen another significant increase in margin in the first two fiscal quarters of 2024, reaching a historic high of over 53%. In the future, it may be important to monitor whether this segment can maintain its current level of competitiveness and profitability.

In conclusion, to fully comprehend Microsoft's recent successful transformations, we need to closely monitor changes in revenue and margins for all three business segments. More Personal Computing can be considered as a "cash cow" but it receives low market attention.

Microsoft's Intelligent Cloud business was once the company's growth engine, but its revenue growth for this fiscal quarter has stabilized and rebounded, with operating margins reaching historic highs. It may be important to monitor whether Microsoft can maintain this rebound in revenue growth and profitability in future financial reports.

In addition, the integration of Copilot has led to significant changes in revenue growth and operating margins for Microsoft's productivity and business processes segment. We need to continue monitoring its sustainability in future financial reports.